How Does Guaranteed Compounding Work?

Every year, guaranteed cash value increases according to the policy contract. Those gains become part of the foundation for future growth.

Instead of starting over each year, the growth builds upon prior growth. As the policy matures, larger cash values create larger opportunities for continued compounding.

This process rewards patience and consistency. Time becomes an ally rather than a source of uncertainty.

Why Does Guaranteed Growth Matter After 50?

Many successful individuals spend decades building businesses, acquiring real estate, and creating wealth. As retirement approaches, preserving what has been built often becomes more important than chasing aggressive returns.

A major market decline near retirement can significantly impact future income plans.

Guaranteed growth provides:

- Greater predictability

- Protection from market volatility

- Confidence in long-term planning

- A stable foundation alongside other assets

For individuals who value certainty and control, guaranteed compounding can play an important role in overall wealth preservation.

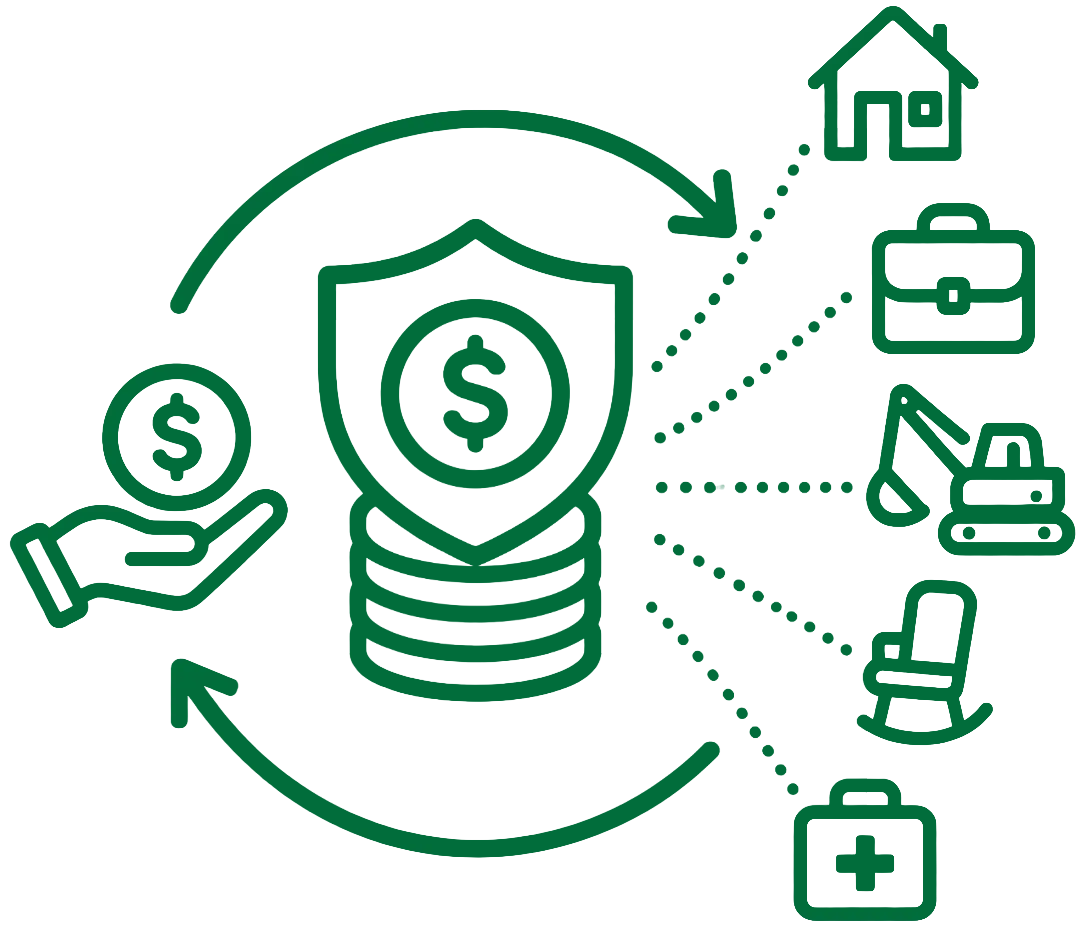

Can You Use Cash Value Without Stopping Growth?

One of the unique features of properly structured participating whole life insurance is the ability to access policy cash value through policy loans while the underlying cash value continues earning growth.

This creates flexibility that many people find attractive.

Potential uses may include:

- Real estate opportunities

- Business expansion

- Equipment purchases

- Liquidity during retirement

- Unexpected expenses

The ability to maintain compounding while accessing capital is one reason many affluent families incorporate this strategy into their financial planning.

Guarantees vs. Projections: What’s the Difference?

Many financial products rely heavily on projections.

A projection illustrates what may happen under certain assumptions. It is not a contractual promise.

A guarantee is different. It is written into the policy contract and backed by the issuing insurance company.

Understanding the distinction is critical when evaluating long-term financial strategies.

Questions to ask include:

- Which values are guaranteed?

- Which values are projected?

- What assumptions support the projections?

- How have guarantees performed historically?

Clear answers help separate certainty from speculation.

How Do Dividends Enhance Guaranteed Growth?

Participating whole life policies issued by qualifying mutual insurance companies may pay dividends.

Dividends are not guaranteed. However, many established mutual companies have long histories of paying them.

When dividends are used to purchase paid-up additions, they can:

- Increase cash value

- Increase death benefit

- Expand future growth potential

- Strengthen long-term compounding

The guarantee creates the foundation. Dividends can enhance the overall growth trajectory over time.

How Do You Verify the Numbers Are Real?

Any financial strategy should be evaluated using actual policy illustrations and carrier documentation.

Important items to review include:

- Guaranteed cash value schedules

- Policy loan provisions

- Dividend assumptions

- Historical carrier performance

- Financial strength ratings

A properly designed policy should provide transparency regarding both guaranteed values and projected values.

The numbers should be supported by contractual documents, not sales presentations alone.

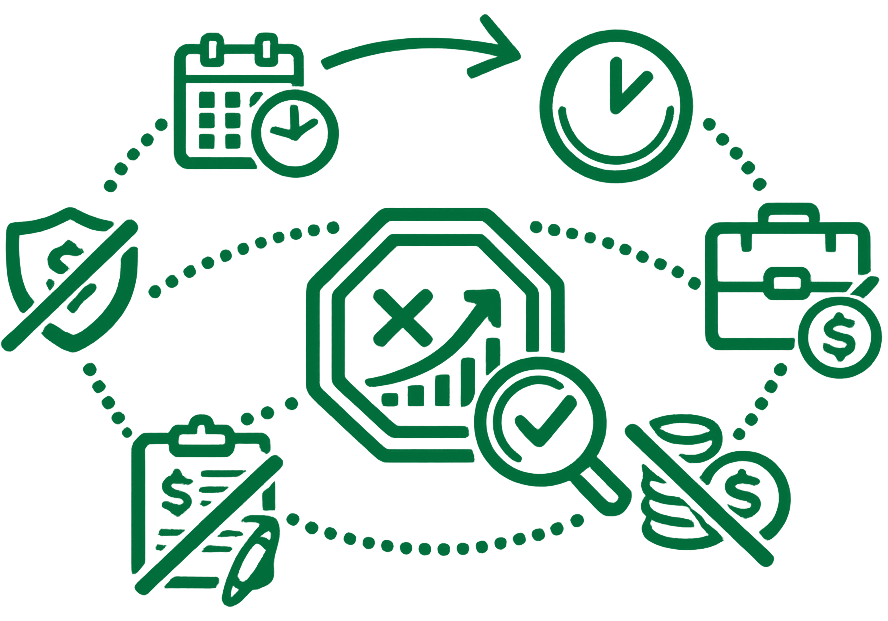

What Mistakes Slow Compounding Growth?

Compounding becomes more powerful when it remains uninterrupted.

Several common mistakes can reduce long-term results:

- Delaying implementation

- Underfunding the policy

- Choosing the wrong policy design

- Working with carriers that lack financial strength

- Treating the policy as a short-term strategy

Small decisions early on can have significant effects decades later.

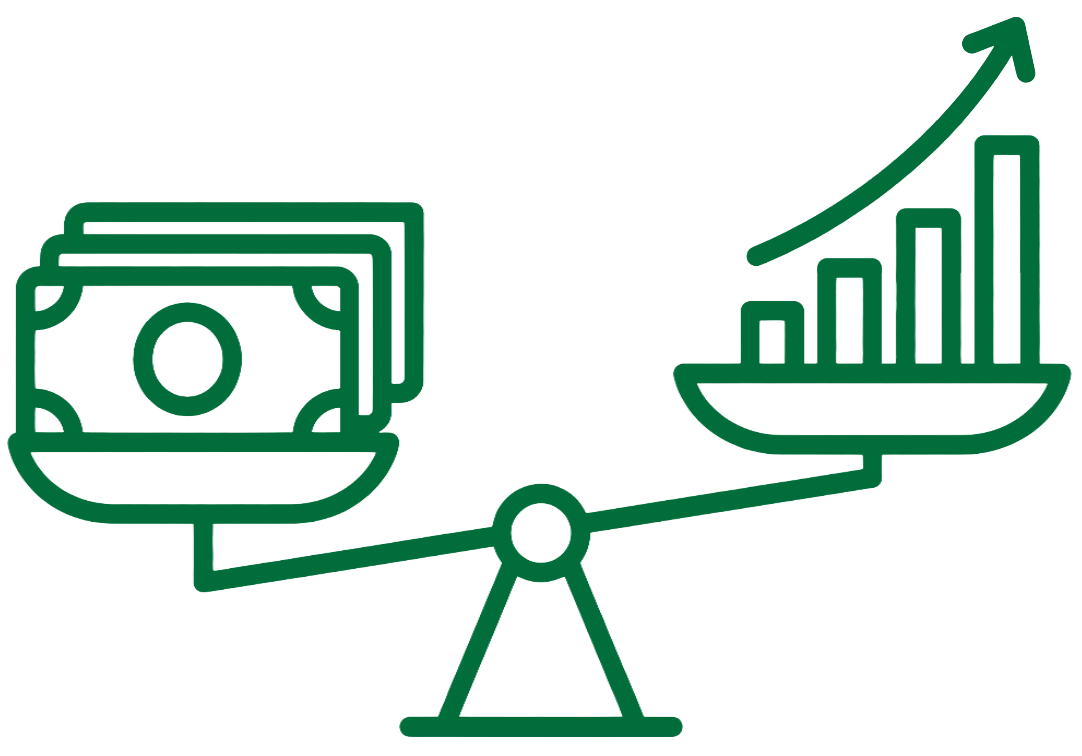

Guaranteed Compounding vs. Cash: Which Wins?

Holding substantial cash reserves may provide comfort and liquidity, but idle cash often struggles to maintain purchasing power over time.

Inflation gradually reduces what those dollars can buy.

Guaranteed compounding creates the potential for:

- Continuous growth

- Increased efficiency of capital

- Greater long-term purchasing power

- Ongoing liquidity through policy access

Cash remains important for day-to-day needs. The question is whether excess capital should remain dormant or continue working.

How Much Does Waiting Cost?

Compounding rewards time.

Every year of delay means one less year of growth building upon growth.

Many people focus on rate of return while overlooking the importance of duration. In reality, the number of years available for compounding often has a greater impact than small differences in performance.

Starting earlier creates more opportunities for growth to accumulate and compound over future decades.

How Strong Must the Insurance Company Be?

The strength of the insurance company matters because guarantees are only as reliable as the carrier behind them.

When evaluating a company, consider:

- Financial strength ratings

- Surplus reserves

- Long-term stability

- Claims-paying ability

- Dividend-paying history

- Mutual company structure when applicable

A strong carrier provides the foundation for the guarantees that make this fifth pillar possible.

Guaranteed compounding is ultimately about creating a financial asset that grows predictably, remains accessible, and can never go backwards due to market declines. For those seeking greater control over their capital, it serves as a cornerstone of a long-term private banking strategy.

Episode 169 – The Tailwind Effect of Private Banking

The average person spends money once. Banks recycle the same dollar repeatedly. That is the difference. The wealthy understand that the real power is not merely earning income — it is controlling the movement of capital. When families reclaim the banking function in their own lives: money continues compounding, liquidity

Episode 157 – Financially Stressed? The “Become Your Own Bank” Strategy They Don’t Teach You

Are you feeling stuck—living paycheck to paycheck, uncertain about your financial future, and watching retirement drift further out of reach? If you’re ready to regain control, eliminate debt, self-finance major purchases, and build a true multi-generational wealth strategy, this episode is your blueprint. In this episode of the Private Banking

Episode 154 – Stop Saving Money: Why the Rich Don’t Rely on Savings Accounts

What does it truly take to build generational wealth that endures for decades? While many families rely on traditional strategies like 401(k)s, IRAs, stocks, and real estate to grow and transfer wealth, few are aware of a time-tested strategy quietly used by affluent families for more than 200 years. In

What Is A Modified Endowment Contract and IBC

A Modified Endowment Contract can quietly change the tax treatment of a whole life policy, making proper design essential to preserve tax-free growth and control within Infinite Banking. By Vance D. Lowe RFC, ChFC, CLU When someone tells me they want to “overfund” a whole life policy for cash

The Ultimate Private Family Banking Guide

A comprehensive guide to structuring a private family banking system that protects capital, generates tax-free growth, and builds a multi-generational financial legacy. By Vance D. Lowe RFC, ChFC, CLU For over four decades in the financial arena, I have watched successful families accumulate substantial wealth—only to leave it exposed

Banking Independence: How to Embrace the Concept of Being Your Own Bank

A clear explanation of banking independence and how reclaiming control of your capital creates protection, efficiency, and a lasting financial legacy. By Vance D. Lowe RFC, ChFC, CLU For most successful individuals, wealth was built through discipline, work ethic, and intelligent risk-taking. Yet ironically, once that wealth is created,